Stock buybacks – also known as share repurchases – are in the news again. In his 2023 State of the Union address in Washington D.C., President Biden proposed quadrupling the recently enacted excise tax1 on corporate stock buybacks. The proposal comes at a time when corporations are ramping up buybacks after pausing in late 2022, with $173.5 billion already planned for this year.2

On August 16, 2022, the Inflation Reduction Act was signed into law, which includes a provision to create a 1% excise tax on share repurchases.3 Diversified investors who own stock likely have some exposure to companies with share repurchase programs in place and will be impacted by the new law, which lawmakers estimate will raise $74 billion over the next ten years.4

Why tax buybacks? Some policymakers appear to hold them in poor regard.5 Unfortunately, public discourse on share repurchases indicates mass confusion on the topic. A few recent articles help to defend buybacks and dispel criticisms about them. For example, see The Case for Stock Buybacks and Buyback Derangement Syndrome.

From a fundamental, economic perspective, dividends and buybacks do not create value for the company or its shareholders. They simply transfer an asset from the company’s balance sheet to the investors who own that company so that it may be more productively redeployed elsewhere. Despite their economic equivalence, buybacks and dividends are taxed differently.

Let’s explore how impactful the newly enacted 1% buyback tax is on after-tax investor outcomes. I believe it will be too modest – about 50 basis points lower after-tax total compound return over a 10-year period – to dissuade companies from continuing to repurchase shares to return cash to investors. Quadrupling the tax approximately quadruples the reduction in after-tax total compound return (it’s still modest) over the 10-year investment period. Below I describe what buybacks are, why they’re useful, and how they’re different than dividends.

What’s a Stock Buyback?

A stock buyback is one approach companies use to distribute cash to investors. A buyback is essentially the opposite of a stock offering, such as an Initial Public Offering (IPO) or Secondary Offering (SO). With IPOs and SOs, companies sell common stock, diluting existing investors, to raise cash. With a share buyback program6, companies repurchase their own shares of common stock, typically on the open market, to reduce excess cash on their balance sheet. Repurchasing shares concentrates equity ownership in remaining investors, reducing the total number of outstanding shares.7

Why Would Companies Repurchase Their Equity?

Companies require capital to fund investment when they are in their growth phase. Later in their lifecycle, they may generate profits more quickly than they can effectively invest in new growth initiatives. Surplus cash on a company’s balance sheet is inefficient and investors should abhor it.

Companies should hold onto what’s required to support business operations, high-returning investments, optionality for future investments, acquisitions, etc., and return the rest to shareholders. In other words, if a company cannot figure out how to deploy cash profitably, it should return that surplus to investors and allow them to do so. A buyback is one such way to accomplish this goal.8

How Does a Buyback Work? An Example

Examples often help illustrate an idea. I build off a simplified version of the example provided in Stock Buybacks for Dummies, but then expand it to compare buybacks to dividends.

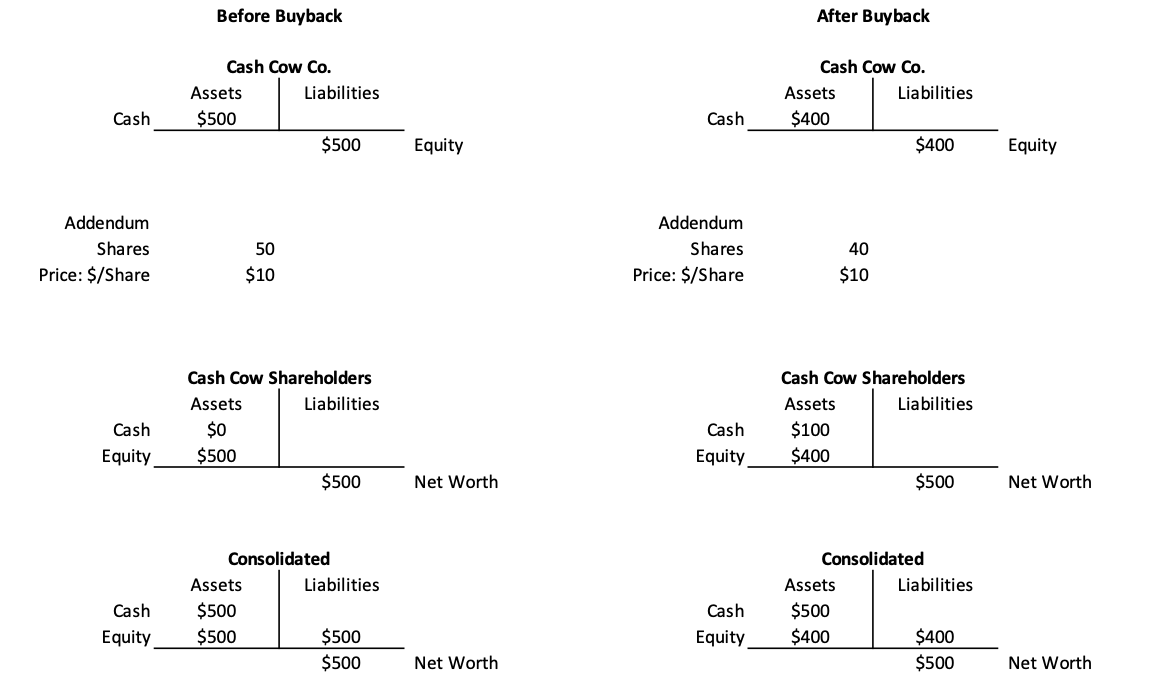

A company, Cash Cow, has $500 of assets with corresponding $500 of equity market value. With 50 shares outstanding, each share has a price of $10. The company seeks to distribute $100 cash to investors through a buyback. It purchases 10 shares at the market price of $10 per share, thereby reducing shares outstanding to 40 shares. After using $100 cash to repurchase and retire equity, Cash Cow has $400 of assets corresponding to $400 of equity market value. With 40 shares outstanding, the fair market price of its shares is unchanged at $10.

This is a rather boring event economically speaking. Shareholder net worth is unchanged. The share price is unchanged. There are no economic profits. There are no tax liabilities generated. $100 moved from Cash Cow’s balance sheet to the investors’ pockets and the company’s market capitalization dropped by the same amount.

However, the buyback did accomplish three things. First, each remaining shareholder’s ownership in the company increased. Before the buyback, with 50 shares outstanding, each share represents 2% ownership in the company. After the buyback, each of the remaining 40 shares outstanding represents 2.5% ownership in the company.

Second, the buyback gave existing investors cash that may be reinvested more productively elsewhere. Cash Cow relinquished control of the $100 they distributed through the buyback. And finally, Cash Cow’s earnings yield will have increased because it generates about the same earnings with a smaller balance sheet.

Figure 1: Buyback example

What About Dividends Instead?

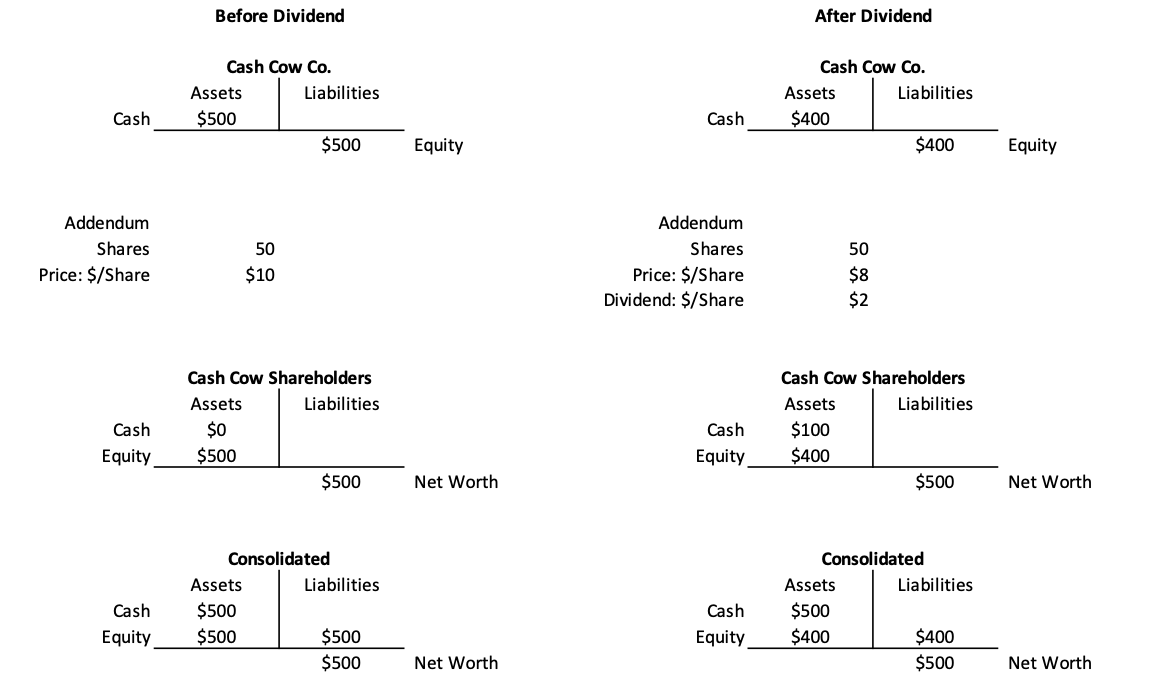

In the above example, Cash Cow distributed $100 via repurchased stock. What if they issued dividends instead? The result, illustrated in Figure 2, is nearly identical to the share buyback.

Another boring event, economically speaking, albeit slightly less so. As in the case of the buyback… Shareholder net worth is unchanged. There are no economic profits. $100 moved from Cash Cow’s balance sheet to the investors’ pockets and the company’s market capitalization dropped by the same amount.

There is however an important difference. Because the shares outstanding are unchanged, the price per share has declined from $10 to $8, the change perfectly offsetting the $2 dividend distribution.9 No economic profit, but an unrealized capital loss of $2 and a realized dividend of $2. This has tax implications!

The investor incurs a tax liability on the $2 dividend. If the investor sells Cash Cow to realize the $2 loss in price, they can use that realized loss to reduce tax liabilities arising from realized capital gains, but they cannot offset the dividend tax liability.10 So, the investor may very well owe a tax despite not having made a cent in profit on their investment.

Figure 2: Dividend Example

Stock Buyback Taxes

The act of distributing cash from a company’s balance sheet to investors does not create economic profit. The value of investors’ holdings, whether distributions occur via dividends or buybacks, is unchanged – at least before taxes enter the picture.

Dividend taxes add confusion. A dividend distribution creates an explicit tax liability, but also an implicit offsetting capital gains tax reduction. They offset, although at different times and at different tax rates, which further adds confusion. Every dollar in dividends received is implicitly accompanied with either a dollar of capital loss or a reduction of a dollar of capital gain.11

It is because dividends lead to offsetting price declines and because capital gains are taxed that dividends also must be taxed. Otherwise, companies can use untaxed dividends to prevent share prices from rising and eliminate capital gains tax liabilities altogether. Dividend taxes prevent this type of tax manipulation, an issue that buybacks do not face.

Like dividends, buybacks do not create any economic gain for an investor. A buyback tax extracts12 money from investors or from companies on an activity that is dissociated from economic profits, with the intention of dissuading the reallocation of capital to more efficient investments, which is why many people find the tax so distasteful.

Impact of Buyback Taxes

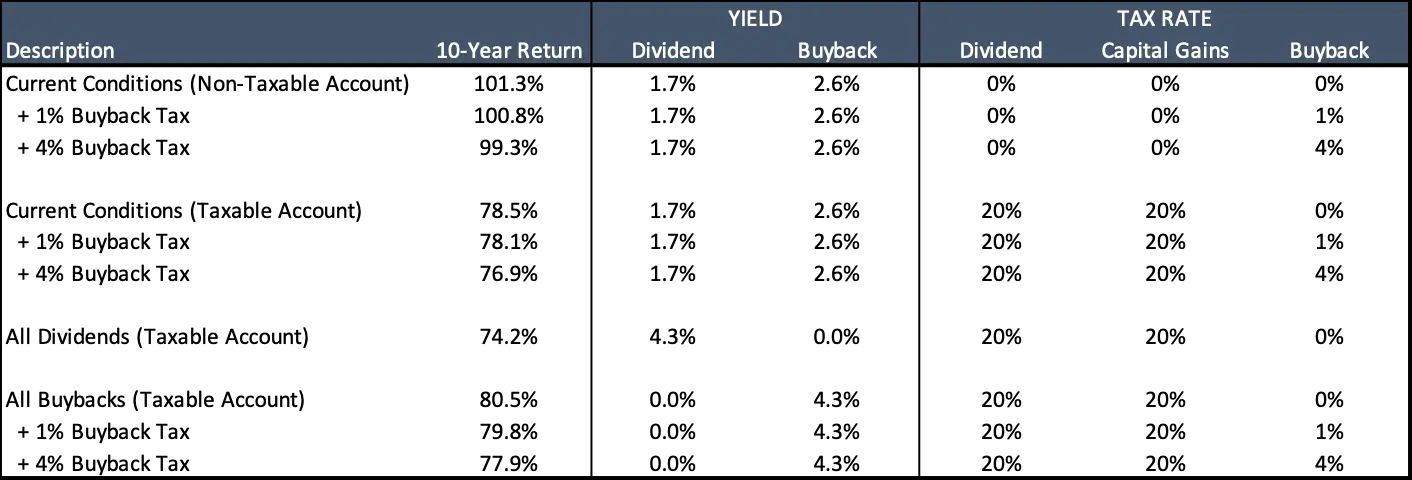

It’s worth exploring how impactful the tax on share repurchases may be on investment outcomes. The good news, for investors at least, is that the expected impact – whether buybacks are taxed at 1% or 4% – is modest. I consider a ten-year investment in equities with 7% annualized return and 16% volatility.13

I assume that dividend taxes are 20%, capital gains taxes are also 20%, and consider share repurchases with the 1% tax and proposed 4% tax. I assume that at the end of the simulation, the equity is liquidated and capital gains taxes are paid on realized gains. My baseline payout yield assumptions are from Yardeni for S&P 500: 1.7% dividend yield and 2.6% buyback yield.

Figure 3: Impact of Buyback Taxes

Figure 3 summarizes the results of my analysis. Over a ten-year period, we expect a 101.3% return gross of tax. There is an interesting impact of the buyback tax. It introduces taxation on investments that exist in non-taxable accounts such as Roth IRAs. Dividends and capital gains are untaxed within these accounts, but a buyback tax paid by the company does effectively flow through to the investor, even in non-taxable accounts. With a 1% tax rate on buybacks, the impact is modest, reducing the total gross return over 10 years from 101.3% to 100.8%. If the newly proposed increase to a 4% tax rate were introduced, the total gross return would further decline to 99.3% assuming no changes in dividend or buyback yield.

What about taxable accounts? Net of tax returns are 78.5%, which is more than 22% below the tax-free 101.3% return, despite dividend and capital gains tax rates of 20%. There are two explanations for the higher effective tax rate: (1) sometimes the investor paid dividend taxes that didn’t net against realized capital losses and (2) dividend taxes paid each year didn’t earn investment income as occurs in a tax-free account – i.e., no tax deferral. A 1% tax on buybacks modestly reduces net of tax returns from 78.5% to 78.1%. Increasing the tax to 4% reduces net of tax returns to 76.9%.

Many policymakers and commentators seem to prefer a move away from buybacks to dividends. What would occur if the entire equity payout yield materialized through dividends with no buybacks? Net of tax returns decline to 74.2%, which is almost 27% below the tax-free total 10-year return. What if the entire payout yield materialized through buybacks with no dividends? Net of tax returns increase to 80.5%.

Here we see the benefits of buybacks vs. dividends. It is often framed that investments with buybacks have lower effective tax rates than investments with dividends. That’s technically true, but framing and anchoring are important. Investments with buybacks have precisely the tax rate intended by the capital gains tax policy. Dividends have had higher effective taxes on total returns than the tax rate on dividends would imply because dividend taxes are paid even when an owner has lost money on their investment.

Finally, in a world in which companies move away from dividends to buybacks, with a 4.3% buyback yield and buybacks are taxed at a 1% rate, the total 10-year return is 79.8%, an effective total tax rate on profits of 21%. Increasing the buyback tax rate to 4% drops the total 10-year net return to 77.9%, which is an effective tax rate on profits of 23.1%. Some have suggested that such a tax would incentivize companies to favor dividends over buybacks. From the taxable investors’ perspective, such a move appears questionable. Investors should expect higher total net of tax returns (and lower total effective tax rates) with buybacks, whether they are taxed at a 1% or even 4%. For this reason, it seems unlikely that such a tax will deter companies from continuing to repurchase shares.

Summary

Buybacks continue to be a source of confusion for many investors, market commentators, and policymakers. They are often described as mechanisms for artificially increasing a company’s share price, and thus a potential source of market manipulation. Financial theory does not support such claims.

Neither buybacks nor dividends create economic profits for investors. They are simply methods for companies to distribute surplus cash to investors. Doing so generally increases earnings yield as the same earnings are delivered with fewer assets. It also enables investors to reinvest cash elsewhere to earn additional returns. It’s unclear why investors should favor policies that discourage companies from returning surplus cash.

All else equal, dividend-paying stocks are less tax-efficient than those that buyback shares. This is because dividends may generate tax liabilities in unprofitable investments and because the benefits of tax deferral are lost. A 1% tax on share repurchases narrows the gap, but only modestly so. Even with such a tax, investors likely continue to benefit when companies choose to return surplus cash and do so using buybacks over dividends. Perhaps the more notable impact of such a policy is that it introduces investment taxes on stocks that are owned in tax-deferred and tax-exempt accounts.

Disclosure

Roni Israelov is President and Chief Investment Officer at NDVR, Inc. E-mail: roni.israelov@ndvr.com.

This material is published for informational purposes only.

The views expressed and other information included are as of the date indicated and based on the data available at that time. They may change based on changes in markets, general economic conditions, rules and regulations, and other factors. NDVR does not assume any duty to update any of the views and information herein. Unless otherwise noted, views and opinions expressed are those of the authors and not necessarily those of NDVR or its affiliates.

NDVR is an investment advisor that may or may not apply the views and other information described herein when providing services to its clients. The views and information herein are not and may not be relied on in any manner as, investment, legal, tax, accounting or other advice provided by NDVR to any individual or entity or as an offer to sell or a solicitation of an offer to buy any security.

Footnotes

-

The excise tax is applied to net buybacks, which is the fair market value of stock less the total fair market value of issuances of stock in the same taxable year (“netting rule”). The Act applies to special classes of stock including non-publicly traded stock and preferred stock, but not to repurchases of stock by Real Estate Investment Trusts.

For more information, see New 1% Excise Tax on Stock Buybacks May Have Far-Reaching Consequences for Capital Markets, SPAC and M&A Transactions. ↩

-

The IRS issued interim guidance to taxpayers on the corporate stock repurchase excise tax here: Treasury, IRS issue guidance on corporate stock repurchase excise tax in advance of forthcoming regulations ↩

-

Democrats add stock buyback tax, scrap carried interest to win Sinema over ↩

-

Although A Stock Buyback Tax Isn’t a Great Idea doesn’t favor the tax, it provides a taste of the distaste some have for buybacks. ↩

-

Like IPOs and SOs, buybacks are approved by a company’s board of directors, after which a buyback announcement news release is issued. ↩

-

With fewer shares outstanding, a company’s earnings and cash flow is distributed to a more concentrated pool of investors. Thus, valuation metrics such as earnings per share (EPS) are typically impacted after a company buys back shares. This has led to a debate on whether companies use buybacks to artificially impact shareholder value. ↩

-

In addition, companies should arguably be free to decide their appropriate capital structure. Some firms finance investment with debt, while others finance investment by issuing additional equity. Companies may later decide that the capital structure that most benefits their investors has changed. Companies may seek to reduce financial leverage by paying back debt, perhaps by issuing additional equity. Other companies may seek to increase financial leverage by issuing debt to buy back stock. These are standard management decisions and share repurchases are one of several tools that companies use to adjust their capital structures. ↩

-

I must acknowledge the ex-dividend date anomaly. Campbell and Beranek (1955) report that prices dropped on average 90% of the dividend paid on ex-dividend dates, 10% short of expectation. Elton and Gruber (1970) report an 80% drop on ex-dividend dates, 20% short of expectation. They suggest that taxes may play a role because – at the time – dividends were taxed at a higher rate than capital gains. ↩

-

Elton and Gruber (1970) investigates the clientele effect arising from marginal investor tax rates. ↩

-

In fact, it’s possible to use this feature to come out ahead. If a stock is held at least 60 days, then its dividend is taxed at the favorable qualified rate of at most 20%. If it is liquidated at a loss and held for under a year, then the capital losses are short-term can offset short-term gains at the ordinary income tax rate. ↩

-

According to the internal revenue code, the corporate tax paid for the amount of stock repurchased is not deductible for federal income tax purposes. ↩

-

My Monte Carlo simulations assume a geometric Brownian motion. ↩